But what has gotten me curious over the past few months is the institutional aspect. In my view, because financial markets are actually populated by institutions that have their own quirks, financial markets can deviate from textbook models in very policy relevant ways.

Most financial models that I have read about are populated by individual investors looking to maximize some expected future consumption stream subject to various constraints. Sometimes these constraints stick to describing feasible budget allocations,and sometimes they also include cognitive biases. But Wall Street doesn't look like this. Traders rarely trade by themselves -- they are usually a part of a large firm. These firms may also have different goals. Some, such as hedge funds, are just in the business of generating pure return whereas others, such as pension funds, are looking to maintain a steady stream of payments to pay out to their customers. Given that these firms have their own institutional demands, this suggests that their trading strategies could be quite different. These structural differences has implications for market efficiency.

Past papers have of course addressed some of these issues. On a within-firm basis, work on the principal-agent problem has shown how compensation schemes can affect fund manager behavior. This would suggest that many financial managers maximize not the utility of the investor, but their payoff in the compensation scheme. Some past work has also indicated that institutional investors, in this case mostly pension funds, do not seem to exhibit the herding and destabilizing behavior that for which they are criticized. However, some of these benign results are being challenged in the recent financial crisis, and this could have major implications for both financial research and monetary policy.

As an example, there have been a set of recent popular articles from the Economist and FT Alphaville on the notion of VAR shocks. VAR is a measure of financial risk that (theoretically) measures the worst case outcome for a firm. For example, a 5% weekly VaR of $5 million means that there should only be a 5% percent chance that the firm will lose more than $5 million over the course of a given week. This typically can be calculated by parameterizing a loss distribution with historical data on volatility and average yields. Even though this measure can mislead by ignoring the amount that would actually be lost in a worst-case outcome its simplicity makes it a natural candidate for institutions to use as a check against overly risky trading strategies. Therefore market moves that can impact the measurement of VAR are natural candidates for making the institutional investors jump.

Pioneering work by Hyun Song Shin, an economist at Princeton, analyzes the role of VAR and argues that it contributes to market procyclicality. Because historical data is used to calculate the VAR that goes into risk weighting, banks may end up levering up their balance sheet just as the business cycle starts to rev up and deleveraging just as the entire cycle comes crashing down. The rising tide of the business cycle makes their VAR look much smaller, therefore allowing them to put smaller risk weights on their assets. Now that the size of risk weighted assets has fallen, banks can play the risk-weighting clause on capital requirements and fund themselves through more debt. This continues until the cycle breaks, at which point VAR measurements are shocked upward by the historical data, forcing a deleveraging in order to meet capital requirements, thereby amplifying negative effects on the business cycle. In particular, this story fits the recent financial crisis very well. Past decades of relative calm made the VAR models docile and ready for the slaughter that was 2008.

I see this as an institutional bug because there’s no efficiency reason why VAR should be used in such a way to risk-weight assets. It does not make for an omniscient Q-measure to identify risk. Rather, VAR is useful because it helps institutions streamline their risk analysis. By doing so, it quite possibly improves an individual firm’s performance by avoiding worse evaluation methods. But with the procyclicality argument made above, it should be clear that a group of banks all using VAR to risk weight their assets end up creating severe negative externalities on the business cycle.

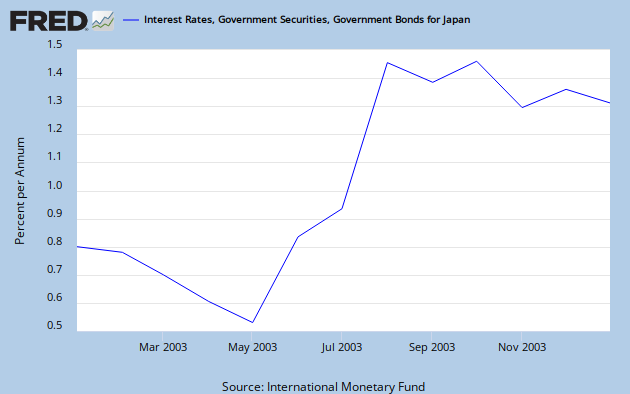

VAR shocks have also popped up in the Japanese case. Back in the 2003 bond yield volatility spike, many Japanese banks ended up selling bonds as the volatility triggered their VAR limits. This intensified the cycle of bond selling until other investors, such as pension funds and insurance companies bought up the bonds and stabilized the market. This serves as another real world example of Shin’s theory that the use of VAR in institutional settings ends up intensifying market volatility.

Most financial models that I have read about are populated by individual investors looking to maximize some expected future consumption stream subject to various constraints. Sometimes these constraints stick to describing feasible budget allocations,and sometimes they also include cognitive biases. But Wall Street doesn't look like this. Traders rarely trade by themselves -- they are usually a part of a large firm. These firms may also have different goals. Some, such as hedge funds, are just in the business of generating pure return whereas others, such as pension funds, are looking to maintain a steady stream of payments to pay out to their customers. Given that these firms have their own institutional demands, this suggests that their trading strategies could be quite different. These structural differences has implications for market efficiency.

Past papers have of course addressed some of these issues. On a within-firm basis, work on the principal-agent problem has shown how compensation schemes can affect fund manager behavior. This would suggest that many financial managers maximize not the utility of the investor, but their payoff in the compensation scheme. Some past work has also indicated that institutional investors, in this case mostly pension funds, do not seem to exhibit the herding and destabilizing behavior that for which they are criticized. However, some of these benign results are being challenged in the recent financial crisis, and this could have major implications for both financial research and monetary policy.

As an example, there have been a set of recent popular articles from the Economist and FT Alphaville on the notion of VAR shocks. VAR is a measure of financial risk that (theoretically) measures the worst case outcome for a firm. For example, a 5% weekly VaR of $5 million means that there should only be a 5% percent chance that the firm will lose more than $5 million over the course of a given week. This typically can be calculated by parameterizing a loss distribution with historical data on volatility and average yields. Even though this measure can mislead by ignoring the amount that would actually be lost in a worst-case outcome its simplicity makes it a natural candidate for institutions to use as a check against overly risky trading strategies. Therefore market moves that can impact the measurement of VAR are natural candidates for making the institutional investors jump.

Pioneering work by Hyun Song Shin, an economist at Princeton, analyzes the role of VAR and argues that it contributes to market procyclicality. Because historical data is used to calculate the VAR that goes into risk weighting, banks may end up levering up their balance sheet just as the business cycle starts to rev up and deleveraging just as the entire cycle comes crashing down. The rising tide of the business cycle makes their VAR look much smaller, therefore allowing them to put smaller risk weights on their assets. Now that the size of risk weighted assets has fallen, banks can play the risk-weighting clause on capital requirements and fund themselves through more debt. This continues until the cycle breaks, at which point VAR measurements are shocked upward by the historical data, forcing a deleveraging in order to meet capital requirements, thereby amplifying negative effects on the business cycle. In particular, this story fits the recent financial crisis very well. Past decades of relative calm made the VAR models docile and ready for the slaughter that was 2008.

I see this as an institutional bug because there’s no efficiency reason why VAR should be used in such a way to risk-weight assets. It does not make for an omniscient Q-measure to identify risk. Rather, VAR is useful because it helps institutions streamline their risk analysis. By doing so, it quite possibly improves an individual firm’s performance by avoiding worse evaluation methods. But with the procyclicality argument made above, it should be clear that a group of banks all using VAR to risk weight their assets end up creating severe negative externalities on the business cycle.

VAR shocks have also popped up in the Japanese case. Back in the 2003 bond yield volatility spike, many Japanese banks ended up selling bonds as the volatility triggered their VAR limits. This intensified the cycle of bond selling until other investors, such as pension funds and insurance companies bought up the bonds and stabilized the market. This serves as another real world example of Shin’s theory that the use of VAR in institutional settings ends up intensifying market volatility.

It should also be clear that the institutional quirks can occur in financial markets with rational arbitrageurs. If the size of institutional flows are large enough, then it may be worthwhile for the smaller traders to just ride the flows to higher returns. There may just not be enough incentive to normalize prices. If the market can stay irrational longer than individuals can stay solvent, then an individual is likely better off to just play along with the market. Given thta we see this kind of serial correlation with hedge funds in the tech bubble, the risk of individuals riding along with the irrationalities of institutions should be taken seriously. In fact, I would go far enough as to argue that the burden of proof is on those who would like to defend their financial models with only individual investors. Given that we know the real world doesn’t work like that, and that this difference can result in dramatically different conclusions, the burden must on the traditionalists to show that models of individual investing can subsume those of institutions in most cases.

To measure these effects and to calibrate new models, attention should be focused on the flow of funds in and out of these institutional investments. This way we could have a better notion of relative size and be able to measure if and how much institutional procyclicality affects markets.

I see two main policy implications of this alternative approach. First, the VAR specific quirks create a further justification for strict capital requirements. Only this way can the risk weighting problem be robustly solved. In terms of monetary policy, a thorough understanding of these institutional quirks can help guide the direction of policy. As monetarism starts to integrate more markets as data points, it becomes more and more important for central bankers to know how to interpret the financial data that comes in. By knowing what’s signal and what’s noise, central banks can better conduct forward looking policy.

In all these examples, we see how institutions -- not individual traders -- can end up driving markets. This marks a departure from traditional finance models in which everybody is just an individual playing the market. It is my hope that this kind of analysis will be useful for understanding causes of market inefficiencies and the optimal framework for financial data in monetary policy.

"Numerous studies in behavioral economics have identified what appear to be deviations from fully efficient markets with rational individuals."

ReplyDeletePerhaps this comment is belated and I might be getting too philosophical (I hope you had a Happy New Year, BTW), but couldn't one make the argument that the definition of "rationality" used in the models found in academic economics are excessively narrow?

Are you tired of seeking loans and Mortgages,have you been turned down constantly By your banks and other financial institutions,We offer any form of loan to individuals and corporate bodies at low interest rate.If you are interested in taking a loan,feel free to contact us today,we promise to offer you the best services ever.Just give us a try,because a trial will convince you.What are your Financial needs?Do you need a business loan?Do you need a personal loan?Do you want to buy a car?Do you want to refinance?Do you need a mortgage loan?Do you need a huge capital to start off your business proposal or expansion? Have you lost hope and you think there is no way out, and your financial burdens still persists? Contact us (gaincreditloan1@gmail.com)

ReplyDeleteYour Name:...............

Your Country:...............

Your Occupation:...............

Loan Amount Needed:...............

Loan Duration...............

Monthly Income:...............

Your Telephone Number:.....................

Business Plan/Use Of Your Loan:...............

Contact Us At : gaincreditloan1@gmail.com

Phone number :+44-75967-81743 (WhatsApp Only)

When It Comes To Personal Loans * Business Loans etc., Contact Us Today Via E-mail: SuiteCapitals@gmail.com ( SuiteCapitals@post.com ) It’s Imperative To Work With The Right Company. We Help You Get The Best Rate For Your Business Loan Regardless Of Your Credit!!! If You Are Looking For A Personal Loans * Business Loans etc., You Have Come To The Right Place. Contact Us Today For More Information Through Via E-mail: SuiteCapitals@gmail.com ( SuiteCapitals@post.com )

ReplyDeleteDo You Need A Loan To Consolidate Your Debt At 1.0%? Or A Personal Loans * Business Loans etc. Interested Parties Should Contact Us For More Information Through Via E-mail: SuiteCapitals@gmail.com ( SuiteCapitals@post.com )

We Offers Financial Consulting To Client, Companies Seeking Debt / Loan Financing And Seeking For Working Capital To Start A New Business Or To Expand Existing Business. Interested Parties Should Contact Us For More Information Through Via E-mail: SuiteCapitals@gmail.com ( SuiteCapitals@post.com )

Kindly write us back with the loan information;

- Complete Name:

- Loan amount needed:

- Loan Duration:

- Purpose of loan:

- City / Country:

- Telephone:

- How Did You Hear About Us:

Do You Need A Loan To Consolidate Your Debt At 1.0%? Or A Personal Loans * Business Loans etc. Interested Parties Should Contact Us For More Information Through Via E-mail: SuiteCapitals@gmail.com ( SuiteCapitals@post.com )

We Offers Financial Consulting To Client, Companies Seeking Debt / Loan Financing And Seeking For Working Capital To Start A New Business Or To Expand Existing Business. Interested Parties Should Contact Us For More Information Through Via E-mail: SuiteCapitals@gmail.com ( SuiteCapitals@post.com )

When It Comes To Personal Loans * Business Loans etc., Contact Us Today Via E-mail: SuiteCapitals@gmail.com ( SuiteCapitals@post.com ) It’s Imperative To Work With The Right Company. We Help You Get The Best Rate For Your Business Loan Regardless Of Your Credit!!! If You Are Looking For A Personal Loans * Business Loans etc., You Have Come To The Right Place. Contact Us Today For More Information Through Via E-mail: SuiteCapitals@gmail.com ( SuiteCapitals@post.com )

ReplyDeleteDo You Need A Loan To Consolidate Your Debt At 1.0%? Or A Personal Loans * Business Loans etc. Interested Parties Should Contact Us For More Information Through Via E-mail: SuiteCapitals@gmail.com ( SuiteCapitals@post.com )

We Offers Financial Consulting To Client, Companies Seeking Debt / Loan Financing And Seeking For Working Capital To Start A New Business Or To Expand Existing Business. Interested Parties Should Contact Us For More Information Through Via E-mail: SuiteCapitals@gmail.com ( SuiteCapitals@post.com )

Kindly write us back with the loan information;

- Complete Name:

- Loan amount needed:

- Loan Duration:

- Purpose of loan:

- City / Country:

- Telephone:

- How Did You Hear About Us:

Do You Need A Loan To Consolidate Your Debt At 1.0%? Or A Personal Loans * Business Loans etc. Interested Parties Should Contact Us For More Information Through Via E-mail: SuiteCapitals@gmail.com ( SuiteCapitals@post.com )

We Offers Financial Consulting To Client, Companies Seeking Debt / Loan Financing And Seeking For Working Capital To Start A New Business Or To Expand Existing Business. Interested Parties Should Contact Us For More Information Through Via E-mail: SuiteCapitals@gmail.com ( SuiteCapitals@post.com )

Do You Need A Loan To Consolidate Your Debt At 1.0%? SuiteCapitals@gmail.com ( SuiteCapitals@post.com ) Or A Personal Loans * Business Loans etc. Interested Parties Should Contact Us For More Information Through Via E-mail: SuiteCapitals@gmail.com ( SuiteCapitals@post.com )

ReplyDeleteWe Offers Financial Consulting To Client, SuiteCapitals@gmail.com ( SuiteCapitals@post.com ) Companies Seeking Debt / Loan Financing And Seeking For Working Capital To Start A New Business Or To Expand Existing Business. Interested Parties Should Contact Us For More Information Through Via E-mail: SuiteCapitals@gmail.com ( SuiteCapitals@post.com )

Do You Need A Loan To Consolidate Your Debt At 1.0%? SuiteCapitals@gmail.com ( SuiteCapitals@post.com ) Or A Personal Loans * Business Loans etc. Interested Parties Should Contact Us For More Information Through Via E-mail: SuiteCapitals@gmail.com ( SuiteCapitals@post.com )

We Offers Financial Consulting To Client, SuiteCapitals@gmail.com ( SuiteCapitals@post.com ) Companies Seeking Debt / Loan Financing And Seeking For Working Capital To Start A New Business Or To Expand Existing Business. Interested Parties Should Contact Us For More Information Through Via E-mail: SuiteCapitals@gmail.com ( SuiteCapitals@post.com )

Do You Need A Loan To Consolidate Your Debt At 1.0%? SuiteCapitals@gmail.com ( SuiteCapitals@post.com ) Or A Personal Loans * Business Loans etc. Interested Parties Should Contact Us For More Information Through Via E-mail: SuiteCapitals@gmail.com ( SuiteCapitals@post.com )

ReplyDeleteWe Offers Financial Consulting To Client, SuiteCapitals@gmail.com ( SuiteCapitals@post.com ) Companies Seeking Debt / Loan Financing And Seeking For Working Capital To Start A New Business Or To Expand Existing Business. Interested Parties Should Contact Us For More Information Through Via E-mail: SuiteCapitals@gmail.com ( SuiteCapitals@post.com )

Do You Need A Loan To Consolidate Your Debt At 1.0%? SuiteCapitals@gmail.com ( SuiteCapitals@post.com ) Or A Personal Loans * Business Loans etc. Interested Parties Should Contact Us For More Information Through Via E-mail: SuiteCapitals@gmail.com ( SuiteCapitals@post.com )

Halo, saya Nyonya Christy Morris, pemberi pinjaman pribadi memberikan kesempatan pinjaman seumur hidup. Apakah Anda memerlukan pinjaman untuk melunasi utang Anda dengan segera atau Anda membutuhkan pinjaman untuk meningkatkan komersial Anda? Apakah Anda telah ditolak oleh bank dan lembaga keuangan lainnya? Kami memberikan pinjaman kepada individu yang membutuhkan bantuan finansial, yang memiliki utang macet atau butuh uang untuk membayar tagihan, kami memberikan pinjaman dengan bunga rendah 2%. Saya ingin menggunakan media ini untuk memberi tahu Anda bahwa kami memberikan bantuan yang dapat dipercaya dan diuntungkan dan akan bersedia menawarkan Anda pinjaman. Jadi hubungi kami hari ini melalui e-mail di: (christymorrisloanfirm@gmail.com)

ReplyDeleteWe Bring To You Good News From Hennager Blank ATM Cards And Bitcoin Investments..

ReplyDeleteHave you been trying to get a real blank ATM Card or bitcoin and it has been a problem trying to get one? Here is Hennager Blank ATM Card easy and affordable to get and it can be delivered to you waiting 24hrs after you have made your order from me at: hennager4040@gmail.com

We have special cash loaded programmed ATM card and bitcoin for you to meet up with those needs of yours and also start up your own business. Our ATM card can be used to withdraw cash at any ATM or swipe, stores and POS. Our cards has daily withdrawal limit depending on the card balance you order.You can make from $2500 to $50,000.00 In USD And EUR,with our Programmed card. Contact us today for your own order at : hennager4040@gmail.com

Here are the price list for ATM Cards:

Balance Price

$2500---------------$155

$5000---------------$255

$10,000-------------$500

$13,000-------------$680

$15,000-------------$760

$17,000-------------$880

$20,000-------------$970

$25,000-------------$1000

$30,000-------------$1100

$35,000-------------$1200

$40,000-------------$1300

$45,000-------------$1350

$50,000-------------$1500

Western Union/Money Gram Transfer

Walmart Transfer

Removing of name from debit record and criminal

Account top-up

Bitcoin Investments

We can also help you hack into any software you wish or want us to hack into too.

Do contact for more info and also on how you are going to get your order..

Order yours today via Email: Gmail-Compose mail to: hennager4040@gmail.com

Hangouts: hennager4040@gmail.com

Hennager Peter.

kesaksian nyata dan kabar baik !!!

ReplyDeleteNama saya mohammad, saya baru saja menerima pinjaman saya dan telah dipindahkan ke rekening bank saya, beberapa hari yang lalu saya melamar ke Perusahaan Pinjaman Dangote melalui Lady Jane (Ladyjanealice@gmail.com), saya bertanya kepada Lady jane tentang persyaratan Dangote Loan Perusahaan dan wanita jane mengatakan kepada saya bahwa jika saya memiliki semua persyarataan bahwa pinjaman saya akan ditransfer kepada saya tanpa penundaan

Dan percayalah sekarang karena pinjaman rp11milyar saya dengan tingkat bunga 2% untuk bisnis Tambang Batubara saya baru saja disetujui dan dipindahkan ke akun saya, ini adalah mimpi yang akan datang, saya berjanji kepada Lady jane bahwa saya akan mengatakan kepada dunia apakah ini benar? dan saya akan memberitahu dunia sekarang karena ini benar

Anda tidak perlu membayar biayaa pendaftaran, biaya lisensi, mematuhi Perusahaan Pinjaman Dangote dan Anda akan mendapatkan pinjaman Anda

untuk lebih jelasnya hubungi saya via email: mahammadismali234@gmail.comdan hubungi Dangote Loan Company untuk pinjaman Anda sekarang melalui email Dangotegrouploandepartment@gmail.com

Ini luar biasa saat saya mengira semua telah selesai dengan saya Ibu Iskandar datang untuk menyelamatkan saya. Saya sangat berhutang sejauh orang-orang yang saya pinjam uang dari geng melawan saya dan kemudian membuat saya ditangkap sebagai akibat dari hutang saya. ditahan selama berbulan-bulan maka masa rahmat diberikan kepada saya saat saya dipulangkan dan dibebaskan untuk pergi dan mencari uang untuk membayar semua hutang yang saya terima sehingga saya diberitahu bahwa ada beberapa kreditur sah online sehingga saya harus mencari Karena melalui blog saya berualang kali tertipu tapi ketika saya menemukan Ibu Iskandar CEO ISKANDAR LESTARI LOAN FIRM, Tuhan mengarahkAan saya ke iklannya melalui blog karena daya tarik saya terhadapnya adalah benar-benar mukjizat mungkin karena Tuhan telah melihat bahwa saya memiliki banyak menderita karena itulah dia mengarahkan saya kepadanya. Jadi saya menerapkannya dengan antusias setelah beberapa jam pinjaman saya disetujui oleh Dewan dan dalam dua hari saya dikreditkan dengana jumlah pasti yang saya berikaan untuk semua ini tanpa jaminan tambahan Kredit Tanpa Agunan (KTA) sama seperti saya berbicara dengan Anda sekarang saya telah dapat menghapus semua hutang saya dan sekarang saya memiliki supermarket sendiri, saya tidak memerlukan bantuan orang lain sebelum saya memberi makan atau mengambil keuangan apa pun keputusan saya tidak punya urusan dengan Polisi lagi saya sekarang adalah wanita merdeka. Anda ingin mengalami kemandirian finansial seperti saya silahkan hubungi Ibu melalui BBM-nya: {D8980E0B} atau melalui email perusahaan: (iskandalestari.kreditpersatuan@gmail.com) Anda tidak dapat memperdebatkan fakta bahwa di dunia kesulitan ini Anda memerlukan seseorang untuk membantu Anda mengatasi gejolak keuangan dalam hidup Anda dengan satu atau lain cara, jadi saya memberi Anda mandat untuk mencoba dan menghubungi Ibu Iskandar di alamat di atas sehingga bisa mengatasi kemerosotan keuangan dalam hidup Anda. Anda bisa menghubungi saya melalui email berikut: (anggaannisa1979@gmail.com)) selalu bersikap positif dengan Ibu Iskandar dia akan melihat Anda melalui semua tantangan finansial Anda dan kemudian memberi Anda sebuah tampilan baru finansial.

ReplyDeleteDetail Kontak Penuh:

Perusahaan: ISKANDAR LESTARI LOAN FIRM (ISKANDAR LENDERS)

Email: {iskandalestari.kreditpersatuan@gmail.com}

Alamat Facebook: {www.facebook.com/iskandar.lesteri.7}

Website: {iskandarlestari.wordpress.com}

TESTIMONI OLEH

Penerima Manfaat: Angga Annisa

Email: {anggaannisa1979@gmail.com}

Twitter: [@AnggaAnnisa1]

ReplyDeleteWe are exclusive agent to direct providers of Fresh Cut BG, SBLC, MTN Bonds, Bank draft and Loans which we have specifically for lease. We do not have any broker chain in this offer or get involved in Chauffer driven offers. We deliver with time and precision as set forth in the agreement. You are at liberty to engage our leased facilities into trade programs as well as in signature project(s) such as Aviation, Agriculture, Petroleum, Telecommunication, construction of Dams, Bridges and any other turnkey project(s) etc.

DESCRIPTION OF INSTRUMENTS:

1. Instrument: Bank Guarantee (BG/SBLC) (Appendix A)

2. Total Face Value: Eur 5M MIN and Eur 10B MAX (Ten Billion USD) .

3. Issuing Bank: HSBC Bank London, Credit Suisse and Deutsche Bank Frankfurt.

4. Age: One Year, One Month

5. Leasing Price: 3% of Face Value plus 2% commission fees to brokers.

6. Delivery: Bank to Bank swift.

7. Payment: MT-103 or MT760

8. Hard Copy: Bonded Courier within 7 banking days.

The Leased Instruments includes: BG’ s, Insurance Guarantees, MTN, ( SBLC) Standby Letters of Credit and Third Party Guarantees such as a standby forward commitment to purchase or a standby loan. If you are a potential Investor or Principle looking to raise capital, we will be happy to answer any questions that you have about this opportunity and to provide you with all the details regarding this services.

Our BG/ SBLC Financing can help you get your project funded, loan financing, please let me know if you are interested in any of our services, by providing you with yearly renewable leased bank instruments. We work directly with issuing bank lease providers, this Instrument can be monetized on your behalf for 100% funding.

BROKERS ARE WELCOME & 100% PROTECTED!!!

We are ready to close leasing with any interested client in few banking days, if interested do not hesitate to contact me direct.

Regards

Philip James

Email: info.frjames1971@gmail.com

Skype: info.frjames1971@gmail.com

We are direct providers of Fresh Cut BG, SBLC and MTN which are specifically for lease/sales, our bank instrument can be engage in PPP Trading, Discounting, signature project(s) such as Aviation, Agriculture, Petroleum, Telecommunication, construction of Dams, Bridges, Real Estate and all kind of projects. We do not have any broker chain in our offer or get involved in chauffeur driven offers. We deliver with time and precision as sethforth in the agreement. Our terms and Conditions are reasonable, below is our instrument description. The procedure is very simple; the instrument will be reserved on euro clear to be verified by your bank, after verification an arrangement will be made for necessary bank documents and stock testing expenses, the cost of the Bank Guarantee/Standby Letter of Credit will be paid after the delivery of the MT760, Description OF INSTRUMENTS: 1. Instrument: Bank Guarantee (BG/SBLC) 2. Total Face Value: Eur/USD 5M MIN and Eur/USD 10B MAX (Ten Billion EURO/USD). 3. Issuing Bank: HSBC Bank London, Barclay's bank London,Credit Suisse and Deutsche Bank Frankfurt. 4. Age: One Year, One Month 5. Purchasing Price: 32% of face value plus 2% commission fees Leasing Price: 4% of Face Value plus 1% commission fees. 6. Delivery: Bank to Bank swift. 7. Payment: MT-103 or MT760 8. Hard Copy: Bonded Courier within 7 banking days. We are ready to close leasing/Buying with any interested client in few banking days, if interested do not hesitate to contact me Name : PAUL DAVID Email: pauldavid20001@gmail.com Skype: P_david123@outlook.com whatsapp:+447921551354

ReplyDeleteWe are direct providers of Fresh Cut BG, SBLC and MTN which are specifically for lease/sales, our bank instrument can be engage in PPP Trading, Discounting, signature project(s) such as Aviation, Agriculture, Petroleum, Telecommunication, construction of Dams, Bridges, Real Estate and all kind of projects. We do not have any broker chain in our offer or get involved in chauffeur driven offers. We deliver with time and precision as sethforth in the agreement. Our terms and Conditions are reasonable, below is our instrument description. The procedure is very simple; the instrument will be reserved on euro clear to be verified by your bank, after verification an arrangement will be made for necessary bank documents and stock testing expenses, the cost of the Bank Guarantee/Standby Letter of Credit will be paid after the delivery of the MT760, Description OF INSTRUMENTS: 1. Instrument: Bank Guarantee (BG/SBLC) 2. Total Face Value: Eur/USD 5M MIN and Eur/USD 10B MAX (Ten Billion EURO/USD). 3. Issuing Bank: HSBC Bank London, Barclay's bank London,Credit Suisse and Deutsche Bank Frankfurt. 4. Age: One Year, One Month 5. Purchasing Price: 32% of face value plus 2% commission fees Leasing Price: 4% of Face Value plus 1% commission fees. 6. Delivery: Bank to Bank swift. 7. Payment: MT-103 or MT760 8. Hard Copy: Bonded Courier within 7 banking days. We are ready to close leasing/Buying with any interested client in few banking days, if interested do not hesitate to contact me Name : PAUL DAVID Email: pauldavid20001@gmail.com Skype: P_david123@outlook.com whatsapp:+447921551354

ReplyDeleteNama saya Rahma Henny dari Ajman di Dubai UAE, saya adalah korban penipuan di tangan pemberi pinjaman, saya ditipu $ 3.000 karena saya membutuhkan pinjaman $ 90.000 untuk modal usaha dan hutang. Saya frustrasi saya tidak punya tempat untuk pergi, dan bisnis saya hancur dalam proses.

ReplyDeleteItu semua terjadi pada bulan Maret 2019, sampai saya bertemu orang-orang daring yang bersaksi tentang pemberi pinjaman nyata Mrs. GRACE ALEXANDER jadi saya mengajukan pertanyaan dan dia memperkenalkan saya kepada seorang ibu GRACE yang baik yang akhirnya membantu saya mendapatkan pinjaman tanpa jaminan $ 90.000 dengan suku bunga rendah. di perusahaan pinjaman GRACE ALEXANDER.

Saya ingin mengambil kesempatan ini untuk berterima kasih kepada Ny. Grace, semoga Tuhan terus memberkati Anda, Ibu Grace atas kejujuran dan perbuatan baik Anda.

Jika Anda membutuhkan pinjaman atau pinjaman tanpa jaminan, segera hubungi ibu Grace dengan mengirim email ke (gracealexanderloancompany@gmail.com)

CEO Tel.: +1(407)792-5682

WhatsApp: +1(407)792-5682

Anda juga dapat menghubungi saya melalui rahmahenny45@gmail.com

PERUSAHAAN PINJAMAN RIKA ANDERSON

ReplyDeleteEmail Perusahaan: rikaandersonloancompany@gmail.com

Perusahaan Whatsapp: +19147057484

Nama: Murniati Sip

Akun Maybank: 514187335011

+60137729440

Email testifier: murniatisip54@gmail.com

Perkenalkan saya Murniati Sip dari Indonesia dan saat ini berada di Penang Malaysia. Saya hanya ingin berbagi pengalaman dengan semua orang yang berada dalam kesulitan, sebelum saya ingin memberi tahu Anda sedikit tentang masalah saya, saya hanya penjual campuran dengan hutang di Maybank Account.

Saya seorang janda dua anak, penghasilan saya hanya bisa digunakan untuk makan, anak saya putus sekolah karena tidak ada biaya, saya stres dan putus asa untuk menjalani hidup saya tetapi setiap kali saya melihat anak saya, saya selalu bersemangat. Saya tidak lupa berdoa dan meminta bantuan Allah.

Saya membuka internet dan secara tidak sengaja saya melihat kesaksian Margaretha Asmaran Via whatsapp +6282340185186 dan email margarethaasmaran@gmail.com tentang pinjaman yang ia dapatkan dari ibu yang jujur RIKA ANDERSON LOAN COMPANY tetapi pada awalnya saya sangat ragu jadi saya menghubungi ibu lain yang juga mendapat pinjaman dari perusahaan yang sama Amalia Anmangkurat melalui telepon dan whatsap +6285964126496 dan email amaliaanmangkurat@gmail.com

Saya akhirnya menghubungi RIKA ANDERSON LOAN COMPANY untuk pinjaman dan setelah sekitar 12 jam, pinjaman saya sebesar RM20.000 dipindahkan ke rekening bank saya. sekarang saya bersyukur bahwa hutang di Bank telah lunas dan saya memiliki usaha yang besar dan anak saya juga bersekolah, terima kasih kepada Allah RIKA PERUSAHAAN PINJAMAN YANG MENDAPATKAN nyata.

SYARIKAT PINJAMAN RIKA ANDERSON

ReplyDeleteE-mel Syarikat: rikaandersonloancompany@gmail.com

Whatsapp Syarikat: +19147057484

Nama: Murniati Sip

Akaun Maybank: 514187335011

+60137729440

E-mel Penguji: murniatisip54@gmail.com

Perkenalkan saya Murniati Sip dari Indonesia dan kini tinggal di Pulau Pinang Malaysia. Saya hanya ingin berkongsi pengalaman dengan semua orang yang menghadapi masalah, sebelum saya ingin memberitahu anda tentang masalah saya, saya hanya penjual bercampur dengan hutang di Akaun Maybank.

Saya seorang janda dua anak, pendapatan saya hanya boleh digunakan untuk makan, anak saya keluar dari sekolah kerana tiada bayaran, saya tertekan dan terdesak untuk menjalani hidup saya tetapi setiap kali saya melihat anak saya, saya sentiasa teruja. Saya tidak lupa berdoa dan meminta bantuan Allah.

Saya membuka internet dan secara tidak sengaja saya melihat keterangan Margaretha Asmaran Via whatsapp +6282340185186 dan email margarethaasmaran@gmail.com tentang pinjaman yang diperolehnya dari seorang ibu yang jujur RIKA ANDERSON LOAN COMPANY tetapi pada mulanya saya sangat ragu-ragu jadi saya menghubungi ibu yang juga mendapat pinjaman dari syarikat yang sama Amalia Anmangkurat atas panggilan dan whatsap +6285964126496 dan e-mel amaliaanmangkurat@gmail.com

Saya akhirnya menghubungi RIKA ANDERSON LOAN COMPANY untuk pinjaman dan selepas kira-kira 12 jam pinjaman saya sebanyak RM20,000 telah dipindahkan ke akaun bank saya. sekarang saya bersyukur bahawa hutang di Bank telah dibayar dan saya berani yang besar dan anak saya juga pergi ke sekolah, terima kasih kepada Allah RIKA ANDERSON LOAN COMPANY adalah nyata.

ReplyDeleteName::::Hafizul Bin Haziq

Country:::Malaysia

Kemarau kewangan saya berakhir pada bulan ini apabila saya fikir semuanya adalah urusan perniagaan dengan beberapa rakan saya di Kuala Lumpur beberapa bulan yang lalu perniagaan yang bernilai beberapa Rm785.000.00 yang keuntungannya sudah cukup untuk kita semua untuk berkongsi keuntungan tetapi akibat kegagalan perniagaan, kita semua mendapati bahawa kita mempunyai masalah kewangan yang sangat besar kerana saya tidak mempunyai wang untuk bergantung pada ketika perniagaan gagal kerana saya melabur semua saya dengan saya pada perniagaan jadi saya berada di sangat sangat maaf jadi saya terpaksa mencari bantuan kewangan saya sebenarnya telah ditolak oleh beberapa bank sebagai hasil dari kadar pinjaman mereka dan juga syarat mereka jadi saya terpaksa melalui beberapa blog sehingga saya datang menghadapi dengan Iklan Syarikat Ibu. saya menghubungi Ibu dengan segera selepas melalui beberapa proses yang sangat fleksibel permintaan pinjaman saya sebanyak Rm440.000.00 telah diluluskan oleh pihak pengurusan dan pada keesokannya Lembaga Pengurusan Peminjaman Pinjaman dikreditkan saya tanpa menangguhkan berkat ini dari ibu yang dapat menyelamatkan anda hari ini dari apa-apa embarrazement kewangan anda menjadi ibu hubungi Ibu sekarang untuk pinjaman anda yang berubah e_mail:[iskandalestari.kreditpersatuan@gmail.com]

ISKANDAR LESTARI LOAN COMPANY "ISKANDAR LENDERS"

[[[[Berikut adalah data peribadi saya]]]]

Country::::::Malaysia

Name::::::::Hafizul Bin Haziq

email::hafizulbin365@gmail.com

Telephone Number:[+60]1123759663

WhatsApp Number::::::::[+60]1123759663

e_mail:[iskandalestari.kreditpersatuan@gmail.com]

PERUSAHAAN PINJAMAN RIKA ANDERSON

ReplyDeleteEmail Perusahaan: rikaandersonloancompany@gmail.com

Perusahaan Whatsapp: +19147057484

Nama: Murniati Sip

Akun Maybank: 514187335011

+60137729440

Email testifier: murniatisip54@gmail.com

Hibah Pinjaman: RM220.000

Perkenalkan saya Murniati Sip dari Indonesia dan saat ini berada di Penang Malaysia. Saya hanya ingin berbagi pengalaman dengan semua orang yang berada dalam kesulitan, sebelum saya ingin memberi tahu Anda sedikit tentang masalah saya, saya hanya penjual campuran dengan hutang di Maybank Account.

Saya seorang janda dari dua anak, penghasilan saya hanya bisa digunakan untuk makan, anak saya putus sekolah karena tidak ada biaya, saya stres dan putus asa untuk menjalani hidup saya tetapi setiap kali saya melihat anak saya, saya selalu bersemangat. Saya tidak lupa berdoa dan meminta bantuan Allah.

Saya membuka internet dan secara tidak sengaja saya melihat kesaksian Margaretha Asmaran Via whatsapp +6282340185186 dan email margarethaasmaran@gmail.com tentang pinjaman yang ia dapatkan dari ibu yang jujur RIKA ANDERSON LOAN COMPANY tetapi pada awalnya saya sangat ragu jadi saya menghubungi ibu lain yang juga mendapat pinjaman dari perusahaan yang sama Amalia Anmangkurat melalui telepon dan whatsap +6285964126496 dan email amaliaanmangkurat@gmail.com

Saya akhirnya menghubungi RIKA ANDERSON LOAN COMPANY untuk pinjaman dan setelah sekitar 12 jam, pinjaman saya sebesar RM20.000 dipindahkan ke rekening bank saya. sekarang saya bersyukur bahwa hutang di Bank telah dilunasi dan saya memiliki usaha yang besar dan anak saya juga bersekolah, terima kasih kepada Allah RIKA PERUSAHAAN PINJAMAN YANG MENDAPATKAN nyata.

Anda semua dipersilakan untuk PERUSAHAAN KREDIT ISKANDAR LESTARI rumah dengan pinjaman besar dan pinjaman ramah pelanggan kami memberikan pinjaman mulai dari miliaran hingga semua calon pelanggan kami dari bagian manapun di dunia dan kami juga ingin Anda semua tahu bahwa kami tidak curang atau menipu pelanggan kami sebagai prioritas utama kami adalah untuk memastikan semua pelanggan kami 100% puas dan senang dengan layanan kami sehingga jumlah minimal yang kami berikan sebagai pinjaman adalah 70juta / RM20679,43 dan maksimumnya adalah dalam miliaran yang berarti Anda dapat juga berlaku dalam miliaran [30 hingga 40 miliar] untuk proyek dan bisnis investasi besar Anda. Kami juga ingin Anda semua mengerti bahwa kami telah menciptakan platform yang mencakup keadaan psikologis pelanggan sehingga pelanggan kami memiliki kesempatan untuk berbicara atau mengobrol dengan staf kami di kantor pusat di Inggris melalui angka-angka yang telah ditampilkan di bawah ini dan juga kepada Manajer Layanan Cabang kami [BSM]

ReplyDeleteKantor pusat:

Tel ::: [+ 44] 7480 729811

W / A Tidak: [+ 44] 7480 729811

Instagram: @Iskandar_Lestari _Loan_Firm

Facebook: https: //www.facebook.com/iskandar.lesteri.7

Web: https: //wordpress.com/view/iskandarlestari.wordpress.com

1] Kantor Cabang:

Manajer Layanan Cabang [B.S.M]

Tel: ☎ [+62] 816-1754-7646

W / A No: [+ 62] 816-1754-7646

Negara: Indonesia

2] Kantor Cabang:

Manajer Layanan Cabang [B.S.M]

Tel:☎ +60 11-2375-9663

W / A No: +60 11-2375-9663

Negara: Malaysia

Courtesy: ISKANDAR LENDERS INC.

Nama Perusahaan::"":":":"ONE BILLION RISING FUNDGmail Perusahaan:":":":":"::"onebillionrisingfund@gmail.com Selamat siang

ReplyDeleteNamaku Nyonya Ahmed Neni dan saya berbicara sebagai salah satu orang paling bahagia di dunia saat ini dan saya mengatakan kepada diri sendiri bahwa pemberi pinjaman yang menyelamatkan keluarga saya dari situasi buruk kami, saya akan menceritakan namanya kepada dunia dan saya sangat bahagia dengan katakan bahwa keluarga saya kembali untuk selamanya karena saya membutuhkan pinjaman sebesar Rp150.000.000.00 untuk memulai hidup saya sejak saya adalah satu ibu dengan 3 anak dan dunia sepertinya sedang bergantung pada saya saat saya mencoba untuk mendapatkan pinjaman Dari bank dan online bank menolak saya pinjaman mereka mengatakan bahwa penghasilan saya rendah dan saya tidak memiliki jaminan untuk pinjaman jadi saya pergi online dan hal-hal menjadi lebih sulit karena mereka merobek uang saya dari saya dengan janji manis untuk membantu saya sampai saya bertemu dengan ALLAH mengirim pinjaman pinjaman yang mengubah hidup saya dan keluarga saya, ONE BILLION RISING FUND dimana Juruselamat ALLAH dikirim untuk menyelamatkan keluarga saya dan pada awalnya saya pikir ini tidak akan mungkin terjadi karena pengalaman masa lalu saya dan janji palsu tapi untuk mengejutkan saya, saya menerima pinjaman saya sebesar Rp150.000.000.00 dan saya akan menyarankan siapa saja yang benar-benar membutuhkan pinjaman untuk menghubungi perusahaan tersebut, melalui email di: """""""onebillionrisingfund@gmail.com"""""""karena mereka adalah pemberi pinjaman yang paling pengertian dan baik hati. Jika Anda melihat bagaimana memastikan pinjaman atau bagaimana mendapatkan pinjaman asli, perusahaan dapat membantu Anda. "

BBM: D8E814FC

Sebagai penerima manfaat dari perusahaan saya adalah bukti hidup dari kerja baik perusahaan dan saya meyakinkan Anda bahwa Anda akan mendapatkan formulir pinjaman ONE BILLION RISING FUND. cukup hubungi mereka dan ikuti proses pemberian pinjaman yang mudah

Anda dapat menghubungi saya Ahmed Neni pada informasi lebih lanjut ((ahmedneni48@gmail.com))

Allahu akbar

(okahomeloanfirm@gmail.com) Baik untuk mempunyai semua orang di sini boleh Tuhan Tuhan yang berkuasa memberkati dan melindungi kita daripada penipu dalam nama jesus amen, saya hanya seorang lelaki muda yang mendapat kelebihan dalam sebuah syarikat yang dipanggil okahome pinjaman syarikat, apabila semuanya bersatu untuk menjadi sangat sukar saya mencari dan pergi ke mana-mana untuk pergi, kemudian saya menolak di nees saya dan berdoa kepada Tuhan, dan loard menjawab saya dengan mengarahkan saya ke syarikat itu, dan saya mempunyai begitu banyak perkara yang saya berfikir dalam saya fikiran, jadi apabila saya sampai di sana, memberi saya hanya merasa langkah untuk mengambil, saya melakukan semua yang saya lakukan, dan saya ditanya berapa banyak yang saya perlukan, dan saya memberitahu mereka berapa banyak yang saya perlukan dan tidak ada masa yang sia-sia mereka mengalihkan saya nombor akaun dan sebelum anda tahu apa yang berlaku, saya mendapat wang pada akaun saya, dan saya adalah shocket, beacouse saya tidak dapat mencatatkan diri saya mempunyai jumlah sebanyak 550 ribu dolar untuk membuat perniagaan saya, selepas itu saya berkata kepada diri saya sendiri bahawa saya harus menceritakan kepada semua orang kisah-kisah, meminta semua orang dapat berlari ke sebuah syarikat pinjaman untuk mengesahkannya sendiri yang terletak di calgary di canada, atau anda juga dapat mengadaptasi saya untuk maklumat lebih lanjut dengan e_mail saya (littledons101@gmail.com) atau anda boleh mengarahkannya langsung di sana melalui e_mail (okahomeloanfirm@gmail.com) bolehkah tuan memberkati syarikat pinjaman okahom bagi saya dalam nama jesus, kawan-kawan yang berkenan tidak ke barat masa anda tempat-tempat lain sila mengamalkannya sekarang dan dapatkan masalah anda diselesaikan

ReplyDeletekota: Balikpapan

ReplyDeletepekerjaan.:::::bisnis

WhatsApp. (* (*) *) * +447723553516

Daftar sekarang: (aasimahaadilaahmed.loanfirm@gmail.com)

Assalamualaikum Warahmatullahi Wabarakatuh

Halo semua, mohon saran Anda semua di sini untuk tidak mengajukan pinjaman di setiap perusahaan pinjaman di situs ini, semua orang di sini adalah palsu dan curang, bahkan beberapa kesaksian di sini semuanya palsu, mereka adalah orang yang sama yang melakukan semuanya,. jadi harap berhati-hati untuk tidak menjadi korban penipuan pinjaman, saya telah ditipu 6 kali dari Rp150 juta untuk semacam biaya transfer, asuransi dan biaya perpajakan, tetapi setelah pembayaran saya saya tidak mendapatkan pinjaman saya, sebaliknya mereka bertanya kepada saya membayar lebih dan lagi. Tetapi Tuhan sangat bersyukur bahwa saya kemudian mendapat pinjaman modal sebesar Rp4,4 miliar dari Perusahaan tempat teman saya bekerja, (AASIMAHA ADILA AHMED LOAN FIRM), mereka adalah perusahaan terkemuka sekarang di Asia, mereka di sini untuk membantu kita semua yang memiliki telah scammed, jadi jika Anda memerlukan pinjaman lebih baik pergi ke kantor perusahaan di UNITED KINGDOM, Mereka memberikan pinjaman besar pinjaman internasional kepada pemilik bisnis di Malaysia dan Indonesia dan di seluruh dunia, mereka sangat cepat dalam pengiriman yang sah, yang sangat sederhana untuk mendapatkan dan hanya 1% tanpa jaminan. saya telah membayar semua hutang pinjaman bank dan bisnis saya dengan baik sekarang. Anda dapat menghubungi mereka baik-baik saja dengan Aplikasi Anda dengan mereka. Anda akan mendapatkan pinjaman dalam 1 jam, saya melakukan semua ini untuk membantu negara saya dari penipuan, dan saya juga membuat beberapa trik cara mengetahui pemberi pinjaman palsu.

BAGAIMANA MENGETAHUI PEMENANG PALSU

Peminjam palsu tidak perlu meminta jaminan dan tidak ada situs web, Peminjam tidak memiliki sertifikat bisnis, Peminjam palsu tidak peduli dengan gaji bulanan Anda yang membuat Anda memenuhi syarat untuk pinjaman, Peminjam palsu tidak menggunakan gmail, tidak ada dominasi,Peminjam palsu tidak memiliki alamat kantor fisik, peminjam palsu meminta biaya pendaftaran dan biaya pajak.

Email; jurjanibude0811@gmail.com

ReplyDeleteemail:::::::hafizulbin365@gmail.com

Name::::Hafizul Bin Haziq

Country:::Malaysia

Kemarau kewangan saya berakhir pada bulan ini apabila saya fikir semuanya adalah urusan perniagaan dengan beberapa rakan saya di Kuala Lumpur beberapa bulan yang lalu perniagaan yang bernilai beberapa Rm785.000.00 yang keuntungannya sudah cukup untuk kita semua untuk berkongsi keuntungan tetapi akibat kegagalan perniagaan, kita semua mendapati bahawa kita mempunyai masalah kewangan yang sangat besar kerana saya tidak mempunyai wang untuk bergantung pada ketika perniagaan gagal kerana saya melabur semua saya dengan saya pada perniagaan jadi saya berada di sangat sangat maaf jadi saya terpaksa mencari bantuan kewangan saya sebenarnya telah ditolak oleh beberapa bank sebagai hasil dari kadar pinjaman mereka dan juga syarat mereka jadi saya terpaksa melalui beberapa blog sehingga saya datang menghadapi dengan Iklan Syarikat Ibu. saya menghubungi Ibu dengan segera selepas melalui beberapa proses yang sangat fleksibel permintaan pinjaman saya sebanyak Rm440.000.00 telah diluluskan oleh pihak pengurusan dan pada keesokannya Lembaga Pengurusan Peminjaman Pinjaman dikreditkan saya tanpa menangguhkan berkat ini dari ibu yang dapat menyelamatkan anda hari ini dari apa-apa embarrazement kewangan anda menjadi ibu hubungi Ibu sekarang untuk pinjaman anda yang berubah e_mail:[iskandalestari.kreditpersatuan@gmail.com]

ISKANDAR LESTARI LOAN COMPANY "ISKANDAR LENDERS"

[[[[Berikut adalah data peribadi saya]]]]

Country::::::Malaysia

Name::::::::Hafizul Bin Haziq

email::hafizulbin365@gmail.com

Telephone Number:[+60]1123759663

WhatsApp Number::::::::[+60]1123759663

e_mail:[iskandalestari.kreditpersatuan@gmail.com]

Nama Perusahaan::"":":":"ONE BILLION RISING FUND

ReplyDeleteGmail Perusahaan:":":":":"::"onebillionrisingfund@gmail.com

Selamat siang

Namaku Nyonya Ahmed Neni dan saya berbicara sebagai salah satu orang paling bahagia di dunia saat ini dan saya mengatakan kepada diri sendiri bahwa pemberi pinjaman yang menyelamatkan keluarga saya dari situasi buruk kami, saya akan menceritakan namanya kepada dunia dan saya sangat bahagia dengan katakan bahwa keluarga saya kembali untuk selamanya karena saya membutuhkan pinjaman sebesar Rp150.000.000.00 untuk memulai hidup saya sejak saya adalah satu ibu dengan 3 anak dan dunia sepertinya sedang bergantung pada saya saat saya mencoba untuk mendapatkan pinjaman Dari bank dan online bank menolak saya pinjaman mereka mengatakan bahwa penghasilan saya rendah dan saya tidak memiliki jaminan untuk pinjaman jadi saya pergi online dan hal-hal menjadi lebih sulit karena mereka merobek uang saya dari saya dengan janji manis untuk membantu saya sampai saya bertemu dengan ALLAH mengirim pinjaman pinjaman yang mengubah hidup saya dan keluarga saya, ONE BILLION RISING FUND dimana Juruselamat ALLAH dikirim untuk menyelamatkan keluarga saya dan pada awalnya saya pikir ini tidak akan mungkin terjadi karena pengalaman masa lalu saya dan janji palsu tapi untuk mengejutkan saya, saya menerima pinjaman saya sebesar Rp150.000.000.00 dan saya akan menyarankan siapa saja yang benar-benar membutuhkan pinjaman untuk menghubungi perusahaan tersebut, melalui email di: """""""onebillionrisingfund@gmail.com"""""""karena mereka adalah pemberi pinjaman yang paling pengertian dan baik hati. Jika Anda melihat bagaimana memastikan pinjaman atau bagaimana mendapatkan pinjaman asli, perusahaan dapat membantu Anda. "

BBM: D8E814FC

Sebagai penerima manfaat dari perusahaan saya adalah bukti hidup dari kerja baik perusahaan dan saya meyakinkan Anda bahwa Anda akan mendapatkan formulir pinjaman ONE BILLION RISING FUND. cukup hubungi mereka dan ikuti proses pemberian pinjaman yang mudah

Anda dapat menghubungi saya Ahmed Neni pada informasi lebih lanjut ((ahmedneni48@gmail.com))

Allahu akbar

Ini luar biasa saat saya mengira semua telah selesai dengan saya Ibu Iskandar datang untuk menyelamatkan saya. Saya sangat berhutang sejauh orang-orang yang saya pinjam uang dari geng melawan saya dan kemudian membuat saya ditangkap sebagai akibat dari hutang saya. ditahan selama berbulan-bulan maka masa rahmat diberikan kepada saya saat saya dipulangkan dan dibebaskan untuk pergi dan mencari uang untuk membayar semua hutang yang saya terima sehingga saya diberitahu bahwa ada beberapa kreditur sah online sehingga saya harus mencari Karena melalui blog saya berualang kali tertipu tapi ketika saya menemukan Ibu Iskandar CEO ISKANDAR LESTARI LOAN FIRM, Tuhan mengarahkAan saya ke iklannya melalui blog karena daya tarik saya terhadapnya adalah benar-benar mukjizat mungkin karena Tuhan telah melihat bahwa saya memiliki banyak menderita karena itulah dia mengarahkan saya kepadanya. Jadi saya menerapkannya dengan antusias setelah beberapa jam pinjaman saya disetujui oleh Dewan dan dalam dua hari saya dikreditkan dengana jumlah pasti yang saya berikaan untuk semua ini tanpa jaminan tambahan Kredit Tanpa Agunan (KTA) sama seperti saya berbicara dengan Anda sekarang saya telah dapat menghapus semua hutang saya dan sekarang saya memiliki supermarket sendiri, saya tidak memerlukan bantuan orang lain sebelum saya memberi makan atau mengambil keuangan apa pun keputusan saya tidak punya urusan dengan Polisi lagi saya sekarang adalah wanita merdeka. Anda ingin mengalami kemandirian finansial seperti saya silahkan hubungi Ibu melalui BBM-nya: {D8980E0B} atau melalui email perusahaan: (iskandalestari.kreditpersatuan@gmail.com) Anda tidak dapat memperdebatkan fakta bahwa di dunia kesulitan ini Anda memerlukan seseorang untuk membantu Anda mengatasi gejolak keuangan dalam hidup Anda dengan satu atau lain cara, jadi saya memberi Anda mandat untuk mencoba dan menghubungi Ibu Iskandar di alamat di atas sehingga bisa mengatasi kemerosotan keuangan dalam hidup Anda. Anda bisa menghubungi saya melalui email berikut: (anggaannisa1979@gmail.com)) selalu bersikap positif dengan Ibu Iskandar dia akan melihat Anda melalui semua tantangan finansial Anda dan kemudian memberi Anda sebuah tampilan baru finansial.

ReplyDeleteDetail Kontak Penuh:

Perusahaan: ISKANDAR LESTARI LOAN FIRM (ISKANDAR LENDERS)

Email: {iskandalestari.kreditpersatuan@gmail.com}

Alamat Facebook: {www.facebook.com/iskandar.lesteri.7}

Website: {iskandarlestari.wordpress.com}

TESTIMONI OLEH

Penerima Manfaat: Angga Annisa

Email: {anggaannisa1979@gmail.com}

Twitter: [@AnggaAnnisa1]

Nama saya Christian Calvin

ReplyDeletePertama-tama saya memuji rasa aman, karena saya telah ditipu online di sini sebelum seorang teman yang mendapat pinjaman menghubungkan saya ke Email: (oliviadaniel93@gmail.com)

Setelah saya menyerahkan salinan kartu identitas dan detail akun saya, pinjaman saya disetujui, itu tidak bisa dipercaya, saya pikir itu akan sama dengan yang lain, yang telah mengambil uang saya dan tidak pernah mendengarnya lagi, saya menerima pinjaman saya sekitar satu jam kemudian, "YA" Saya dipanggil oleh bank saya bahwa ada setoran di akun saya.

Mereka nyata, yang perlu Anda lakukan adalah mengikuti instruksi dan proses aplikasi

Perusahaan adalah perusahaan yang baik, mereka membantu saya ketika saya membutuhkan uang, itu sebabnya saya bersaksi tentang perbuatan baik mereka .. tolong ketika Anda akhirnya mendapatkan pinjaman Anda pastikan bahwa Anda juga memberi tahu orang-orang tentang kerja bagus perusahaan ini. , sehingga mereka tidak akan menjadi korban di tangan orang-orang palsu dan tidak berperasaan, yang menyebut diri mereka sebagai pemberi pinjaman perusahaan sementara mereka hanya menipu dan meningkatkan rasa sakit pada orang-orang.

Jadi saya menyarankan semua orang di sini yang membutuhkan pinjaman untuk menghubungi Mrs OLIVIA DANIEL: (oliviadaniel93@gmail.com)

Anda dapat menghubungi saya melalui gmail: (christiancalvin200@gmail.com) jika Anda memerlukan informasi lebih lanjut

Lingkaran cahaya,

ReplyDeleteSaya Annabelle Johnson Saya ingin menerima kerja baik Tuhan dalam hidup saya kepada rakyat saya mencari pinjaman di Asia dan bahagian lain perkataan, kerana ekonomi yang buruk di beberapa negara.

Saya kini tinggal di jakarta di sini di indonesia. Saya seorang Janda dengan empat orang anak dan saya terjebak dalam keadaan kewangan pada bulan Julai 2017 dan saya perlu membiayai semula dan membayar bil saya.

Saya mangsa penipuan kredit 4 kredit, saya kehilangan banyak wang kerana saya sedang mencari pinjaman daripada syarikat mereka. Saya hampir mati dalam proses kerana saya ditangkap oleh orang-orang dari diri saya sendiri, sebelum saya dibebaskan dari penjara dan rakan-rakan saya menerangkan keadaan saya dan kemudian memperkenalkan saya kepada syarikat pinjaman yang dipercayai oleh GLOBAL FINANCE LIMITED.

Bagi orang yang mencari pinjaman? Oleh itu, anda perlu berhati-hati kerana banyak syarikat di internet adalah penipuan di sini, tetapi mereka masih sangat nyata dalam syarikat pinjaman palsu.

Saya mendapat pinjaman dari GLOBAL FINANCE LIMITED Rp500.000.000 dengan mudah dalam tempoh 24 jam selepas saya memohon, maka saya memutuskan untuk menerima kerja baik Allah melalui GLOBAL FINANCE LIMITED dalam kehidupan keluarga saya. Saya dengan senang hati menasihati anda jika anda perlukan dan sila hubungi GLOBAL FINANCE LIMITED. Hubungi mereka melalui e-mel :. (augustaibramhim11@gmail.com)

Anda juga boleh menghubungi saya melalui e-mel saya di (annabellej24johnson111@gmail.com) jika anda merasa sukar atau ingin.

KAMI TAWARKAN SEMUA JENIS PINJAMAN - BERLAKU UNTUK PINJAMAN TERJANGKAU.

ReplyDeleteApakah Anda mencari pinjaman? Anda berada di tempat yang tepat untuk solusi pinjaman Anda di sini! Global Finance Limited memberikan pinjaman kepada perusahaan dan individu dengan tingkat bunga rendah dan terjangkau 2%. untuk semua staf atau orang, silakan hubungi kami untuk bantuan keuangan segera atau strees, kami bangga dengan komitmen kami kepada pelanggan kami; Harus diakui, pinjaman pribadi, pinjaman mobil, pinjaman bisnis / investasi, pinjaman jangka pendek untuk mulai berpikir tentang mendapatkan pinjaman? Apakah Anda serius memerlukan pinjaman mendesak untuk memulai bisnis Anda sendiri? Apakah Anda berhutang? Ini adalah kesempatan Anda untuk mencapai keinginan Anda, kami memberikan pinjaman pribadi, pinjaman dan bisnis pinjaman perusahaan dan semua jenis pinjaman, Anda dapat menghubungi kami di pinjaman yang terjangkau sekarang

hubungi kami.

Alamat email: augustaibramhim11@gmail.com

Saya minta maaf atas apa yang telah Anda lalui sebelumnya, menginfeksi itu salah satu masalah di tangan pemberi pinjaman palsu, Apakah Anda seorang pria atau wanita bisnis? Apakah Anda dalam kekacauan keuangan atau Apakah Anda perlu dana untuk memulai bisnis Anda sendiri? Apakah Anda memerlukan pinjaman untuk memulai Skala Kecil dan bisnis menengah yang bagus? Apakah Anda memiliki skor kredit yang rendah dan Anda kesulitan mendapatkan pinjaman modal dari bank lokal dan lembaga keuangan lainnya? Pelamar yang tertarik harus Hubungi kami melalui email:

Alamat email: augustaibramhim11@gmail.com

DATA APLIKASI

1) Nama Lengkap:

2) Negara:

3) Alamat:

4) Negara:

5) Seks:

6) Status perkawinan:

7) Pekerjaan:

8) Nomor Telepon:

9) Posisi saat ini di tempat kerja:

10) Penghasilan bulanan:

11) Jumlah pinjaman yang dibutuhkan:

12) Durasi pinjaman:

13) Tujuan pinjaman:

14) Agama:

15) Sudahkah Anda melamar sebelumnya:

16) Tanggal Lahir:

Saya ingin Anda tahu bahwa ALLAH tidak akan membiarkan orang-orang baik kelaparan tetapi dia akan tetap jahat dari apa yang mereka inginkan.

Saya ingin Anda tahu bahwa perusahaan ini adalah perusahaan asli dengan rekam jejak yang baik. Saya juga ingin memberi tahu Anda bahwa kami tidak pernah terlibat dalam aktivitas penipuan apa pun. dan saya dapat meyakinkan Anda bahwa apa yang perusahaan lain tidak bisa lakukan untuk Anda, saya akan melakukannya untuk Anda, dan saya akan membuat Anda bahagia dan membuat senyum di wajah Anda baik-baik saja. saya beri Anda kata-kata saya hanya percaya kepada saya dan Anda tidak akan menyesal melakukan bisnis dengan kami, mencari lebih banyak, karena kami di sini untuk menangani semua masalah keuangan Anda, sesuatu dari masa lalu.

Saya dapat meyakinkan Anda 100% bahwa kami adalah perusahaan yang dapat diandalkan yang sedang menyiapkan skema dalam bentuk akuisisi Pinjaman untuk membantu berbagai individu serta organisasi yang memiliki niat merenovasi, utang? Apakah Anda memerlukan pinjaman darurat untuk membayar hutang Anda, atau apakah Anda memerlukan pinjaman untuk meningkatkan bisnis Anda? Apakah Anda ditolak oleh bank dan lembaga keuangan lainnya? Apakah Anda memerlukan konsolidasi atau pinjaman hipotek? refinancing? dan juga pendirian pakaian bisnis. Saya seorang wanita bisnis internasional dan Pemberi Pinjaman yang telah menawarkan Pinjaman kepada perorangan dan perusahaan di Eropa, Asia, Afrika, dan bagian lain dunia.

Pinjaman kami diasuransikan dengan baik untuk keamanan maksimum adalah prioritas kami, tujuan utama kami adalah untuk membantu Anda mendapatkan layanan yang Anda pantas, Program kami adalah cara tercepat untuk mendapatkan apa yang Anda butuhkan dalam sekejap. Kurangi pembayaran Anda untuk mengurangi beban pengeluaran bulanan Anda. Dapatkan fleksibilitas yang dapat Anda gunakan untuk tujuan apa pun mulai dari liburan, pendidikan, hingga pembelian unik. Pelamar yang tertarik harus Hubungi kami melalui email:

Nyonya Augusta Ibramhim GCF

Alamat email: augustaibramhim11@gmail.com

e_mail:[iskandalestari.kreditpersatuan@gmail.com]

ReplyDeleteWhatsApp Number::::::::::[+60]1123759663

email:::::::hafizulbin365@gmail.com

Name::::Hafizul Bin Haziq

Country:::Malaysia

Kemarau kewangan saya berakhir pada bulan ini apabila saya fikir semuanya adalah urusan perniagaan dengan beberapa rakan saya di Kuala Lumpur beberapa bulan yang lalu perniagaan yang bernilai beberapa Rm785.000.00 yang keuntungannya sudah cukup untuk kita semua untuk berkongsi keuntungan tetapi akibat kegagalan perniagaan, kita semua mendapati bahawa kita mempunyai masalah kewangan yang sangat besar kerana saya tidak mempunyai wang untuk bergantung pada ketika perniagaan gagal kerana saya melabur semua saya dengan saya pada perniagaan jadi saya berada di sangat sangat maaf jadi saya terpaksa mencari bantuan kewangan saya sebenarnya telah ditolak oleh beberapa bank sebagai hasil dari kadar pinjaman mereka dan juga syarat mereka jadi saya terpaksa melalui beberapa blog sehingga saya datang menghadapi dengan Iklan Syarikat Ibu. saya menghubungi Ibu dengan segera selepas melalui beberapa proses yang sangat fleksibel permintaan pinjaman saya sebanyak Rm440.000.00 telah diluluskan oleh pihak pengurusan dan pada keesokannya Lembaga Pengurusan Peminjaman Pinjaman dikreditkan saya tanpa menangguhkan berkat ini dari ibu yang dapat menyelamatkan anda hari ini dari apa-apa embarrazement kewangan anda menjadi ibu hubungi Ibu sekarang untuk pinjaman anda yang berubah e_mail:[iskandalestari.kreditpersatuan@gmail.com]

ISKANDAR LESTARI LOAN COMPANY "ISKANDAR LENDERS"

[[[[Berikut adalah data peribadi saya]]]]

Country::::::Malaysia

Name::::::::Hafizul Bin Haziq

email::hafizulbin365@gmail.com

Telephone Number:[+60]1123759663

WhatsApp Number::::::::[+60]1123759663

e_mail:[iskandalestari.kreditpersatuan@gmail.com]

Pendudukan: Harta Tanah / perhotelan

ReplyDeletekedudukan: Pengarah Urusan

Nama: Najwa Mohammed

Bandar: Miri

Pinjaman saya mendapat: Rm 1.5 juta

kadar faedah: 1%

E-mel saya: najwamohammed369@gmail.com

Halo, saya mengucapkan terima kasih kepada allah almight untuk kebaikan dan keberkasaan yang saya dapatkan dari AASIMAHA ADILA LOAN FIRM tahun ini 2020, saya ingin kita medium ini membiarkan muslim saya di malaysia, Tahun lepas saya telah memohon pinjaman banyak kali dan saya bodoh , Tahun ini ketika saya sedang menonton berita perniagaan saya di Aljazeera, saya melihat nama AASIMAHA ADILA AHMED LOAN FIRM pada wawancara menerangkan pakej mereka dan bagaimana mereka memberi pinjaman dan dana amal kepada mereka yang ingin memulakan perniagaan tahun ini. Oleh itu, saya mendengar dan menghubungi mereka dengan kenalan mereka di televisyen, saya memohon Rm 1.5 juta, pada kadar 1% dan pinjaman saya telah diluluskan dan saya mendapat pinjaman saya semudah mungkin. Saya mendapat pinjaman saya dan melabur lebih jauh ke hartanah suami saya. suami saya dari indonesia, banjir yang terjejas rumah keluarga kami di jakarta, sejak kami mendapat pinjaman, kami telah memperbaiki banyak hal dan membayar hutang bank juga.Jika anda ingin perusahaan pinjaman yang nyata dan sah, anda bebas memohon sekarang dan dapatkan pinjaman anda .Mengingatkan diri anda untuk menjadi kuat dan tidak pernah berputus asa. Semakin banyak anda jatuh, semakin kuat anda menjadi bangun. Jangan pernah menyerah tidak kira apa. Buat janji kepada impian anda seolah-olah anda berjanji kepada anak anda. Saya berharap anda lebih besar tahun. Mungkin allah memberkati mereka allah

MOHON SEKARANG

E-mail****aasimahaadilaahmed.loanfirm@gmail.com

Whatsapp **** + 447723553516

KABAR BAIK !!! KABAR BAIK !!! KABAR BAIK !!!

ReplyDeleteKesaksian: Merpati Darma

Alamat: Kota Depok di Indonesia

BRI- Rp350.000.000 juta

merpatidarma@gmail.com

LENDER: PERUSAHAAN PINJAMAN RIKA ANDERSON

Situs web: rikaandersonloancompany.webs.com

Email: rikaandersonloancompany@gmail.com

Panggilan Saluran Bantuan Layanan Pelanggan: +1 (518) 360-2491

Layanan Pelanggan Whatsapp: +15183602491

Nama saya Merpati Darma, dari kota Depok di Indonesia, saya seorang Muslim yang taat, saya ingin menggunakan media ini untuk membagikan kesaksian sejati hidup saya dan sekali lagi mengingatkan semua orang di sini yang hanya ingin mengajukan pinjaman untuk menghubungi Ibu RIKA ANDERSON, permata langka dan ibu yang baik hati yang meminjamkan saya pinjaman tanpa jaminan ketika saya mengajukan pinjaman ke RIKA ANDERSON LOAN COMPANY, karena dia meminjamkan pinjaman saya sebesar Rp350 juta dan kehidupan saya dan seluruh keluarga saya telah berubah secara finansial.

Saya sekarang memiliki bisnis sendiri di kota, melunasi hutang saya, keluarga saya bahagia dan anak-anak saya di sekolah yang baik, beberapa bulan yang lalu, saya mengalami kesulitan keuangan dan karena kebutuhan mendesak saya untuk mendapatkan pinjaman, saya tertipu oleh sebuah perusahaan pinjaman.

Saya kehilangan harapan sampai hari yang setia ini saya sedang memeriksa blog pinjaman dan saya menemukan kesaksian yang murah hati dari ibu Sharifah Isfahann melalui email sharifahisfahann54@gmail.com PERUSAHAAN PINJAMAN RIKA ANDERSON dan saya memutuskan untuk menghubungi ibu Rika Anderson melalui email untuk pinjaman dan setelah mengikuti kebijakan perusahaan saya juga menghubungi Farah Agungs di email farahagungs@gmail.com, pinjaman saya disetujui dan diproses dengan baik dan dalam waktu kurang dari 2 jam saya menerima Rp350 juta di rekening bank saya.

Jadi saya mendorong sesama orang Indonesia dan Asia yang membutuhkan pinjaman untuk menghubungi PERUSAHAAN PINJAMAN RIKA ANDERSON.

Pendudukan: Harta Tanah / perhotelan

ReplyDeletekedudukan: Pengarah Urusan

Nama: Najwa Mohammed

Bandar: Miri

Pinjaman saya mendapat: Rm 1.5 juta

kadar faedah: 1%

E-mel saya: najwamohammed369@gmail.com

Halo, saya mengucapkan terima kasih kepada allah almight untuk kebaikan dan keberkasaan yang saya dapatkan dari AASIMAHA ADILA LOAN FIRM tahun ini 2020, saya ingin kita medium ini membiarkan muslim saya di malaysia, Tahun lepas saya telah memohon pinjaman banyak kali dan saya bodoh , Tahun ini ketika saya sedang menonton berita perniagaan saya di Aljazeera, saya melihat nama AASIMAHA ADILA AHMED LOAN FIRM pada wawancara menerangkan pakej mereka dan bagaimana mereka memberi pinjaman dan dana amal kepada mereka yang ingin memulakan perniagaan tahun ini. Oleh itu, saya mendengar dan menghubungi mereka dengan kenalan mereka di televisyen, saya memohon Rm 1.5 juta, pada kadar 1% dan pinjaman saya telah diluluskan dan saya mendapat pinjaman saya semudah mungkin. Saya mendapat pinjaman saya dan melabur lebih jauh ke hartanah suami saya. suami saya dari indonesia, banjir yang terjejas rumah keluarga kami di jakarta, sejak kami mendapat pinjaman, kami telah memperbaiki banyak hal dan membayar hutang bank juga.Jika anda ingin perusahaan pinjaman yang nyata dan sah, anda bebas memohon sekarang dan dapatkan pinjaman anda .Mengingatkan diri anda untuk menjadi kuat dan tidak pernah berputus asa. Semakin banyak anda jatuh, semakin kuat anda menjadi bangun. Jangan pernah menyerah tidak kira apa. Buat janji kepada impian anda seolah-olah anda berjanji kepada anak anda. Saya berharap anda lebih besar tahun. Mungkin allah memberkati mereka allah

MOHON SEKARANG

E-mail****aasimahaadilaahmed.loanfirm@gmail.com

Whatsapp **** + 447723553516

e_mail:[iskandalestari.kreditpersatuan@gmail.com]

ReplyDeleteWhatsApp Number::::::::::[+60]1123759663

email:::::::hafizulbin365@gmail.com

Name::::Hafizul Bin Haziq

Country:::Malaysia

[[[[di atas adalah data peribadi saya]]]]]

Kemarau kewangan saya berakhir pada bulan ini apabila saya fikir semuanya adalah urusan perniagaan dengan beberapa rakan saya di Kuala Lumpur beberapa bulan yang lalu perniagaan yang bernilai beberapa Rm785.000.00 yang keuntungannya sudah cukup untuk kita semua untuk berkongsi keuntungan tetapi akibat kegagalan perniagaan, kita semua mendapati bahawa kita mempunyai masalah kewangan yang sangat besar kerana saya tidak mempunyai wang untuk bergantung pada ketika perniagaan gagal kerana saya melabur semua saya dengan saya pada perniagaan jadi saya berada di sangat sangat maaf jadi saya terpaksa mencari bantuan kewangan saya sebenarnya telah ditolak oleh beberapa bank sebagai hasil dari kadar pinjaman mereka dan juga syarat mereka jadi saya terpaksa melalui beberapa blog sehingga saya datang menghadapi dengan Iklan Syarikat Ibu. saya menghubungi Ibu dengan segera selepas melalui beberapa proses yang sangat fleksibel permintaan pinjaman saya sebanyak Rm440.000.00 telah diluluskan oleh pihak pengurusan dan pada keesokannya Lembaga Pengurusan Peminjaman Pinjaman dikreditkan saya tanpa menangguhkan berkat ini dari ibu yang dapat menyelamatkan anda hari ini dari apa-apa embarrazement kewangan anda menjadi ibu hubungi Ibu sekarang untuk pinjaman anda yang berubah e_mail:[iskandalestari.kreditpersatuan@gmail.com]

ISKANDAR LESTARI LOAN COMPANY "ISKANDAR LENDERS"

[[[[Berikut adalah data peribadi saya]]]]

Country::::::Malaysia

Name::::::::Hafizul Bin Haziq

email::hafizulbin365@gmail.com

Telephone Number:[+60]1123759663

WhatsApp Number::::::::[+60]1123759663

e_mail:[iskandalestari.kreditpersatuan@gmail.com]

"wa-Alaikumussalam wa-Rahmatullah,"

ReplyDeleteCERITA KEHIDUPAN BENAR

Saya terkenal sebagai Mikhail Irfan Aqil seorang bapa, suami, saudara lelaki dan rakan saya dari (Putrajaya) Malaysia dan saya telah mengalami banyak tekanan kewangan dan tidak ada yang dapat meminjam wang saya untuk menyelesaikan projek perniagaan saya bermula beberapa bulan lalu . Saya telah ditipu oleh beberapa agen palsu yang mendakwa mereka dapat membekalkan saya dengan bahan mentah untuk pengeluaran

Saya menjadi fraustrasi dan jika tidak untuk isteri saya, saya akan melakukan perbuatan bunuh diri kerana kesakitan itu terlalu banyak dan semua harapan hilang yang membuat saya mula hidup dari awal lagi dan ia tidak mudah sehingga saya bertemu ONE BILION RISING FUND sebuah syarikat pinjaman

Saya memutuskan untuk memohon pinjaman selepas saya menghubungi penguji syarikat yang sebenarnya memberi saya harapan dan memberitahu saya tidak tpo takut bahawa syarikat itu akan meminjamkan wang saya selagi saya boleh memberikan mereka requiremet yang merupakan beberapa maklumat peribadi dan saya lakukan jadi selepas saya melalui semua proses yang mereka meminjamkan wang mereka kemudian memberitahu saya bahawa saya telah dijumpai layak untuk pinjaman dan diminta untuk menunggu dan kejutan saya geatest saya mendapat dikreditkan dan ini membuat hidup saya lebih baik hidup dan dan sangat berterima kasih kepada Allah, Isteri saya dan kepada ONE BILLION RISING FUND

GMAIL "" "" "onebillionrisingfund@gmail.com

UNTUK MENGHUBUNGI AKU

Mikhail Irfan Aqil

mikhailirfanaqil@gmail.com

IG :: Mikhail Irfan

Halo semuanya, saya Rika Nadia, saat ini tinggal orang Indonesia dan saya warga negara, saya tinggal di JL. Baru II Gg. Jaman Keb. Lama Utara RT.004 RW.002 No. 26. Saya ingin menggunakan media ini untuk memberikan saran nyata kepada semua warga negara Indonesia yang mencari pinjaman online untuk berhati-hati karena internet penuh dengan penipuan, kadang-kadang saya benar-benar membutuhkan pinjaman , karena keuangan saya buruk. statusnya tidak begitu baik dan saya sangat ingin mendapatkan pinjaman, jadi saya jatuh ke tangan pemberi pinjaman palsu, dari Nigeria dan Singapura dan Ghana. Saya hampir mati, sampai seorang teman saya bernama EWITA YUDA (ewitayuda1@gmail.com) memberi tahu saya tentang pemberi pinjaman yang sangat andal bernama Ny. ESTHER PATRICK Manajer cabang dari Access loan Firm, Dia adalah pemberi pinjaman global; yang saya hubungi dan dia meminjamkan saya pinjaman Rp600.000.000 dalam waktu kurang dari 12 jam dengan tingkat bunga 2% dan itu mengubah kehidupan seluruh keluarga saya.

ReplyDeleteSaya menerima pinjaman saya di rekening bank saya setelah Nyonya. LADY ESTHER telah mentransfer pinjaman kepada saya, ketika saya memeriksa saldo rekening bank saya dan menemukan bahwa jumlah Rp600.000.000 yang saya terapkan telah dikreditkan ke rekening bank saya. dan saya punya buktinya dengan saya, karena saya masih terkejut, emailnya adalah (ESTHERPATRICK83@GMAIL.COM)

Jadi untuk pekerjaan yang baik, LADY ESTHER telah melakukannya dalam hidup saya dan keluarga saya, saya memutuskan untuk memberi tahu dan membagikan kesaksian saya tentang LADY ESTHER, sehingga orang-orang dari negara saya dan kota saya dapat memperoleh pinjaman dengan mudah tanpa stres. Jadi, jika Anda memerlukan pinjaman, hubungi LADY ESTHER melalui email: (estherpatrick83@gmail.com) silakan hubungi LADY ESTHER Dia tidak tahu bahwa saya melakukan ini tetapi saya sangat senang sekarang dan saya memutuskan untuk memberi tahu orang lain tentang dia, Dia menawarkan semua jenis pinjaman baik untuk perorangan maupun perusahaan dan juga saya ingin Tuhan memberkati dia lebih banyak,

Anda juga dapat menghubungi saya di email saya: (rikanadia6@gmail.com). Sekarang, saya adalah pemilik bangga seorang wanita bisnis yang baik dan besar di kota saya, Semoga Tuhan Yang Mahakuasa terus memberkati LADY ESTHER atas pekerjaannya yang baik dalam hidup dan keluarga saya.

Tolong lakukan dengan baik untuk meminta saya untuk rincian lebih lanjut tentang Ibu dan saya akan menginstruksikan, dan ada bukti pinjaman, hubungi LADY ESTHER melalui email: (estherpatrick83@gmail.com) Terima kasih semua

WhatsApp Number::::::::[+60]1123759663

ReplyDeleteName::::Hafizul Bin Haziq

Country:::Malaysia

Kemarau kewangan saya berakhir pada bulan ini apabila saya fikir semuanya adalah urusan perniagaan dengan beberapa rakan saya di Kuala Lumpur beberapa bulan yang lalu perniagaan yang bernilai beberapa Rm785.000.00 yang keuntungannya sudah cukup untuk kita semua untuk berkongsi keuntungan tetapi akibat kegagalan perniagaan, kita semua mendapati bahawa kita mempunyai masalah kewangan yang sangat besar kerana saya tidak mempunyai wang untuk bergantung pada ketika perniagaan gagal kerana saya melabur semua saya dengan saya pada perniagaan jadi saya berada di sangat sangat maaf jadi saya terpaksa mencari bantuan kewangan saya sebenarnya telah ditolak oleh beberapa bank sebagai hasil dari kadar pinjaman mereka dan juga syarat mereka jadi saya terpaksa melalui beberapa blog sehingga saya datang menghadapi dengan Iklan Syarikat Ibu. saya menghubungi Ibu dengan segera selepas melalui beberapa proses yang sangat fleksibel permintaan pinjaman saya sebanyak Rm440.000.00 telah diluluskan oleh pihak pengurusan dan pada keesokannya Lembaga Pengurusan Peminjaman Pinjaman dikreditkan saya tanpa menangguhkan berkat ini dari ibu yang dapat menyelamatkan anda hari ini dari apa-apa embarrazement kewangan anda menjadi ibu hubungi Ibu sekarang untuk pinjaman anda yang berubah e_mail:[iskandalestari.kreditpersatuan@gmail.com]

ISKANDAR LESTARI LOAN COMPANY "ISKANDAR LENDERS"

Country::::::Malaysia

Name::::::::Hafizul Bin Haziq

email::hafizulbin365@gmail.com

Telephone Number:[+60]1123759663

WhatsApp Number::::::::[+60]1123759663

e_mail:[iskandalestari.kreditpersatuan@gmail.com]

Saya Suryanto dari Indonesia di Kota Palu, saya mencurahkan waktu saya di sini karena janji yang saya berikan kepada LADY ESTHER PATRICK yang kebetulan adalah Tuhan yang mengirim pemberi pinjaman online dan saya berdoa kepada TUHAN untuk dapat melihat posisi saya hari ini.

ReplyDeleteBeberapa bulan yang lalu saya melihat komentar yang diposting oleh seorang wanita bernama Nurul Yudianto dan bagaimana dia telah scammed meminta pinjaman online, menurut dia sebelum ALLAH mengarahkannya ke tangan Mrs. ESTHER PATRICK. (ESTHERPATRICK83@GMAIL.COM)

Saya memutuskan untuk menghubungi NURUL YUDIANTO untuk memastikan apakah itu benar dan untuk membimbing saya tentang cara mendapatkan pinjaman dari LADY ESTHER PATRICK, dia mengatakan kepada saya untuk menghubungi Lady. Saya bersikeras bahwa dia harus memberi tahu saya proses dan kriteria yang dia katakan sangat mudah. dari Mrs. ESTHER, yang perlu saya lakukan adalah menghubunginya, mengisi formulir untuk mengirim pengembalian, mengirim saya scan kartu identitas saya, kemudian mendaftar dengan perusahaan setelah itu saya akan mendapatkan pinjaman saya. . Lalu saya bertanya kepadanya bagaimana Anda mendapatkan pinjaman Anda? Dia menjawab bahwa hanya itu yang dia lakukan, yang sangat mengejutkan.

Saya menghubungi Mrs ESTHER PATRICK dan saya mengikuti instruksi dengan hati-hati untuk saya, saya memenuhi persyaratan mereka dan pinjaman saya disetujui dengan sukses tetapi sebelum pinjaman dipindahkan ke akun saya, saya diminta membuat janji untuk membagikan kabar baik tentang Mrs. ESTHER PATRICK dan itulah mengapa Anda melihat posting ini hari ini untuk kejutan terbesar saya, saya menerima peringatan Rp350.000.000. jadi saya menyarankan semua orang yang mencari sumber tepercaya untuk mendapatkan pinjaman untuk menghubungi Mrs. ESTHER PATRICK melalui email: (estherpatrick83@gmail.com) untuk mendapatkan pinjaman yang dijamin, Anda juga dapat menghubungi saya di Email saya: (suryantosuryanto524@gmail.com)

Dear Sir,

ReplyDeleteWe are Titanium Trading Ltd with UK Company RegistrationN0: 09298674. We are the owner and seller of Gold Bullion Bar,Gold Dore Bar and Rough Diamond in small and large quantities.

We are searching for customers /representatives/ brokers/ sellers or buyers mandates who can help us establish a medium of getting to our customers all over the world.Please, if you are interested in transacting Gold Bullion Bar,Gold Dore Bar and Rough Diamond business kindly contact us via our email address for our FCO as we are ready to sign a long lasting gold supply contract with the end buyers World wide.We are also in Joint Venture (JV) with a financial instrument provider company for BG,SBLC,MT109,MT799,MT760,discounting and project funding.In addition,we have an excellent professional relationship with many banks,stock brokers, financial institutions and consultants all over the globe. We have a proven track record of Excellence, speed and reliability. Accept our kindest regards as we move your business to the next level. Our banks will send pre advice without any upfront charges for Purchase and Lease. So if you have any gold bullion buyers that is looking for BG/SBLC,DLC/LC provider that will issue him BG/SBLC to buy our gold bullion, let us know for more details as our Joint Venture(JV)financial instrument company will handle the same.We will be glad to share our working procedures with you upon request to help us proceed towards closing deals effectively.

David Ashley Robert Meadows

Barking House Fardon Road,Market

Harborough, Leicestershire,LE16 United Kingdom

Email.: customersinfo4ttl@gmail.com

Contact Phone No: +447452391978

WhatsApp No: +447924339472